min read

An escalating cost-of-living crisis is set to create critical challenges for the Consumer Technology Durables sector both now, and in the months ahead.

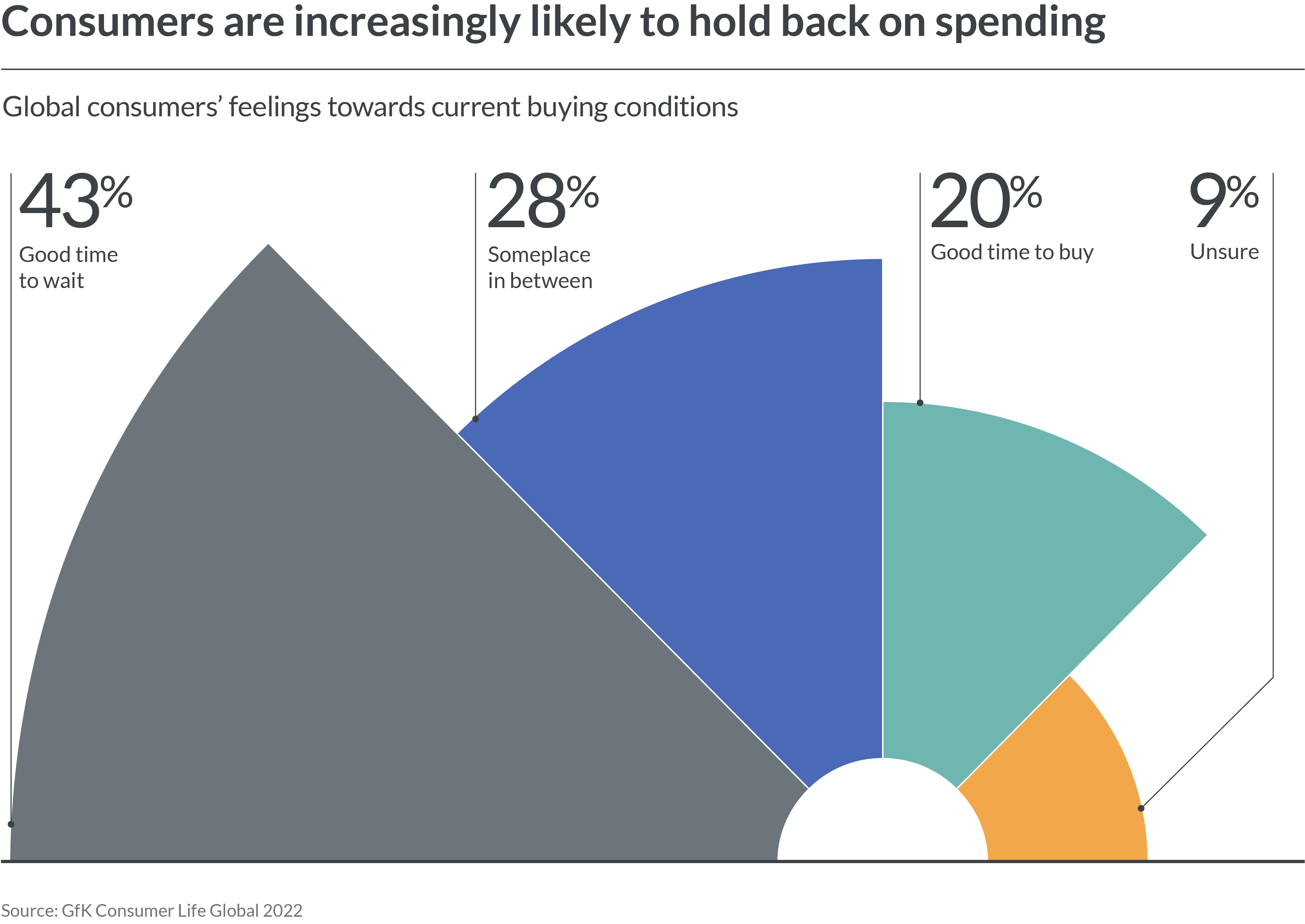

Facing higher household bills and hikes in interest rates, many consumers are consciously cutting back on their spending. Only one fifth consider now a good time to make a purchase, with a far higher proportion opting to wait until more favorable economic conditions return.

This is contributing to a sector-wide slowdown. In H1 2022, total sales values in Consumer Technology and Durables declined by 5.5% compared with the same period of 2021, leaving business decision makers with an uphill battle in securing much-needed value and volume growth. This is even more pertinent for brands and retailers operating in non-urgent sub-categories, such as entertainment and photographic equipment.

So, what strategies can business decision makers use to mitigate this tough economic backdrop?

One option is to take another look at distribution, and consider whether there’s scope to establish or grow market penetration in those countries less exposed to inflationary pressures. Or more specifically, pivot focus from saturated markets mired by high inflation to those with lower durable goods penetration, which are less impacted by high inflation. In time, these markets could become new avenues for growth.

Expanding global market penetration

The sector slowdown is not affecting all regions equally, with a clear split emerging between developed and developing economies.

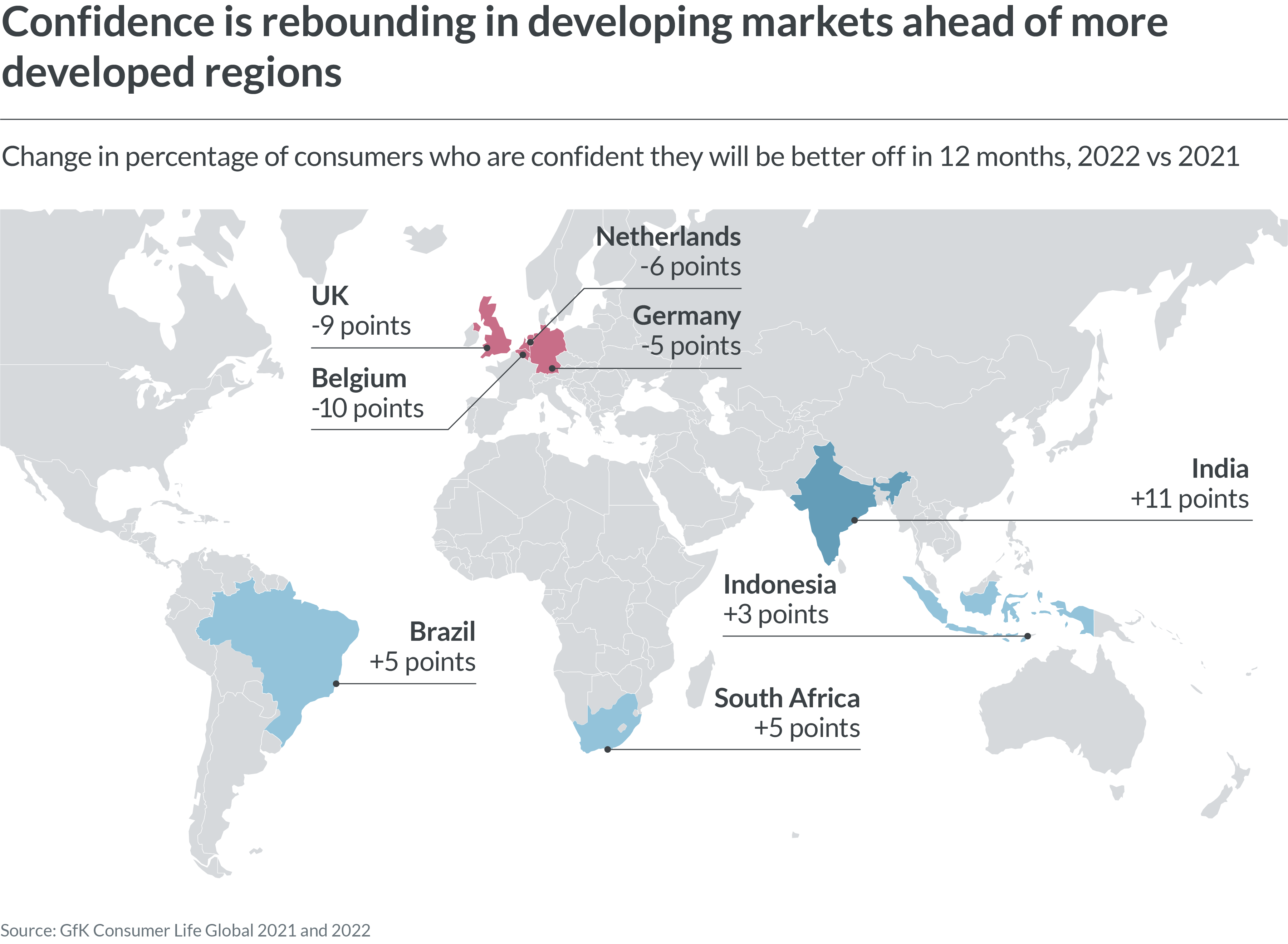

There are significant variations in post-COVID recoveries, supply disruption and inflationary pressures. As a result, consumer confidence has been impacted differently. In the UK for example, the share of consumers confident they’d be financially better off in 12 months fell by nine percentage points from 2021 to 2022. In India though, this proportion increased by 11 percentage points in the same time period. Though higher interest rates did see the Asian economy miss the forecasted GDP growth of 15.2% from April to June this year, it still grew by 13.5% as both agriculture and manufacturing continued to rebound after the pandemic. This left consumers far more confident of a positive trajectory in the year ahead.

Varying consumer confidence is further compounded by vastly different market penetration rates of Consumer Technology and Durables devices. More than 72% of households owned a washing machine in Portugal, Italy, Spain, Germany and the UK as of 2021, for instance, a figure which falls to just 20% in India. This creates clear scope for brands and retailers to bolster value growth through targeting first-time purchasers in the country, rather than attempting to convince consumers in developed markets that now is the time to upgrade or replace their existing device.

In short, there’s an opportunity for the sector to offset some of its losses in developed markets, with a boost to market penetration in developing economies elsewhere in the world.

Understanding new markets

Where brands and retailers do take the step of widening their focus to these developing markets, they’ll need to ensure they adapt their product portfolio, pricing, promotional pricing strategies and brand positioning strategies according to purchasing power and key products relevant in the region.

That means they’ll first need to invest time and resources into building awareness of their brand and launching with messaging tailored to that particular market.

This could mean first forging strategic partnerships or joint ventures with domestic operators that know and understand the market and have already established trust with consumers there. Doing so mitigates the risk of a solo launch and allows brands and retailers to test the market prior to a national rollout.

“Leadership teams should also consider gathering in-depth market insights on macro trends, consumer segmentation and purchase behaviors prior to any launch, in order to adjust their approach accordingly,” advises Namrata Gotarne, Global Strategic Insights Director at GfK. As explored above for example, while in developed markets consumers are often upgrading or replacing existing devices, in developing countries with far lower market penetration rates, they may often be purchasing a device for the first time. “This may require brands and retailers to supply detailed information on the functions and features of a device, as well as its overall ‘use case’ in order to convince a buyer of its value,” she adds.

There may also be a need to widen distribution, with the development of more localized or diversified distribution hubs and production sites, for example, to keep supply consistent. Though a longer-term brand strategy, companies may consider this in the context of serving new markets, given the ongoing volatility in global supply chains.

What should brands and retailers take into account?

Given all these complex considerations, a pivot to developing economies may not be a strategy that works for all brands and retailers within Consumer Technology and Durables.

But for those business decision makers with the capacity to implement such a change, the rewards may be significant. A consumer base far more confident about their financial future, coupled with far lower market penetration rates, creates a clear opportunity for teams to tap into new sources of value growth while facing challenging conditions in their existing markets.

For a detailed look at other strategies brands and retailers can explore against a tough economic backdrop, download our latest State of Consumer Technology and Durables report.

The data in this article has been collected from GfK Market Intelligence: Sales Tracking and GfK Consumer Life Global.