min read

What is driving increasing numbers of people to opt for smart devices as alternatives to the standard version? We investigate the core purchase trends within the global smart home market, why smart products are selling, where the growth opportunities lie, and what brands can do to overcome shoppers’ remaining barriers to maximize that growth.

by Nevin Francis

The penetration of smart products is rising steadily, although smart portfolios overall are not yet mass market in the majority of product categories. The expectation for this year is that these smart portfolios will outperform the market average for their categories as innovation offered by smart portfolio will justify the premium pricing. This premium pricing would be crucial for the manufacturers to secure margins in a tough year mired by demand deceleration. This is because smart products play directly into three of the overarching themes that are driving consumer purchase decisions over the next year – Performance, Simplification and Premiumization. While the long-term potential for the smart market is promising, brands will need precise targeting in the short term, to counter the growing challenges of consumers battling inflation.

The smart home market today

Familiarity with the term ‘smart home’ is growing. Taking a look at some lead markets like UK, for example, 8 out of 10 people now say that they have some knowledge or know a lot about what ‘smart home’ means – up from 6 out of 10 in 2016. In the Netherlands, too, 7 in 10 know exactly or roughly what ‘smart home’ means – up from 6 in 10 in 2018.

When it comes to ownership, UK, China, Italy, Spain and Denmark stand above the global average for the percentage of population owning some form of smart device – and this appetite is increasing.

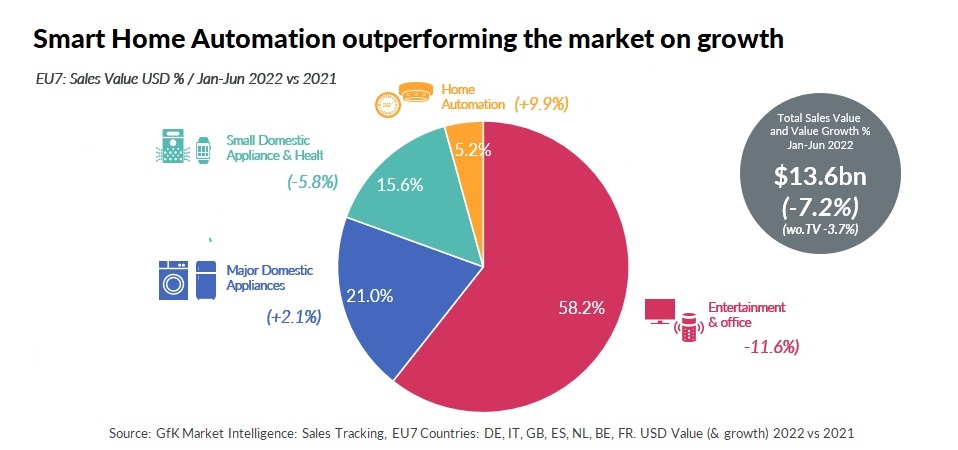

Between January and June this year, sales of smart products brought in 13.6 billion USD across seven major European markets (Belgium, France, Germany, Great Britain, Italy, Netherlands, Spain). This is actually -7.2% down on the same period 2021, or -3.7% down if we exclude smart TVs.

Home entertainment and office is still the biggest share category, accounting for 58.2% of the overall smart market value (due to smart TVs) in these countries for the first half of the year. However, the home automation and major domestic appliances categories saw the best year-to-date growth in H1 2022, standing at +9.9% and +2.1% respectively.

This shows the strength of smart portfolio despite a demand deceleration and lower consumer confidence which plagues the market at large (currently standing at minus 17 in July 2022, which is 27 percentage points lower than in February 2022, for EU27).

Alt text: Data chart showing sales value and growth of key segments of the smart home market for EU7 countries, Jan-Jun 2022

Who are smart home buyers?

A recent study identified two of the three psychological aspects that mark out someone with an affinity for buying into the smart home lifestyle. Those are people who value high social status or real life practicality.

Globally, men are still slightly more likely to buy smart products than women, but the difference is slight. That universal appeal is also seen across age groups. Taking the UK as an example of a leading market, the level of ownership is very similar across those aged 16 to 54, with between 37-40% owning three or more smart devices. It is only for in those aged 55+ that the level of ownership significantly drops, particularly for owning multiple products. Overall, the smart products that are most commonly owned in the UK market are TVs, speakers, fitness & activity trackers and thermostats.

A key variation found in the recent study mentioned above was that the chief attraction of smart products differs across age groups. Those in their 20s say it’s the excitement of owning new technology, while the over-45s focus more on the improved performance that these products bring.

What’s selling and why

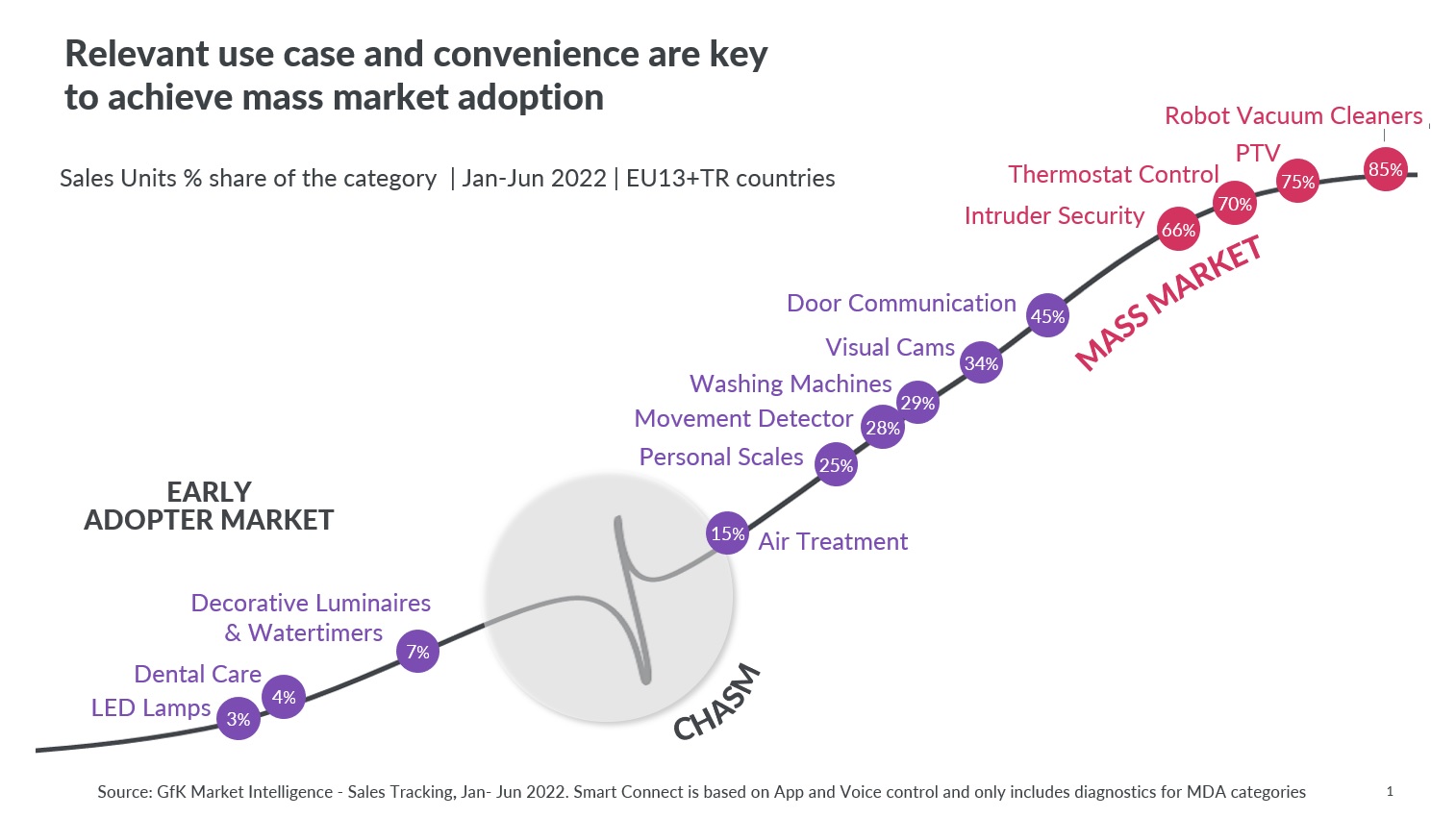

The make-or-break factors for mass adoption of smart alternatives to traditional products is that the smart option presents a strong and relevant ‘use case’ (i.e. it delivers a useful benefit in user’s everyday life) and also delivers increased convenience.

Prime examples of this range from robot vacuum cleaners, where smart versions accounted for 85% unit share of their category last year, through TVs and thermostat control (both around 70%), to intruder security (61%).

By comparison, smart LED lamps have either not convinced consumers that they deliver enough practical benefit over the traditional item, or it is not simple enough to derive benefits This leads to smart portfolio share staying low at 3% in value for H1 this year compared to H1 2021. This may seem surprising, given that consumers say two of the most important smart home use cases are optimizing energy use and remotely monitoring appliances, lights and electronics.

What it boils down to is this: the marketing messaging has not been strong enough to overcome certain existing barriers. These include people not believing that smart LED lamps will significantly help them save energy, and also that the convenience factor of being able to control their lamps remotely is low down on their scale of needs. So, the use case is just not strong enough in people’s current lifestyles.

Alt text: Chart showing where different smart home market products lie on the adoption curve between early adopter and mass market.

Another example that must be included in any analysis of successful smart devices is voice activated speakers or “virtual assistants”. Despite rising concern over privacy and security issues, and awareness of issues around smart speakers. Adoption of smart speakers continues to rise. The secret is that these items have secured a central place inside people’s daily routines. Almost three quarters of people who own a smart or voice-activated speaker say they use it often as part of their daily routine – with the top activities being still basic like playing music, finding out about the weather or news or topics searched, and using it to call or text someone. Also, according to a Google study, the majority keep their speaker in one of the ‘focus’ areas of their home: over half keep it in the living room, and a quarter have it in the kitchen.

Top barriers holding back shoppers

Price

Of the 10 barriers to smart home adoption that we track, price continues to be the number one. This remains the case even for high income consumers, and across genders, generations, and educational levels. Part of the reason for the success of smart speakers is that the category offers some very affordable options. This helps draw in first-time users from consideration to making that first crucial purchase, increasing the pool of familiarity, awareness, and recommendation. We are now seeing cases where, after using very basic smart speakers, consumers are upgrading to higher-end smart speakers from established audio brands.

Privacy

This is another core obstacle. While they are attracted to the convenience and enhanced performance that smart devices can offer, over half of all consumers globally also have concerns about fraudulent use of their personal information, or their privacy being jeopardized. When this is put into the context of smart devices inside their home, those concerns can overcome the benefits offered by smart devices and become a barrier to purchase. This is especially true for smart speakers. Following wide publicity of hackers breaching smart cameras around the home, and smart speakers passively monitoring in-home conversations to acquire user data, some consumers feel the risk is too high to justify the benefit.

Apathy

The next highest barrier is simple lack of interest. The sense of “I don’t see the need for it” and that the benefit is not that compelling. This is where focusing and effectively communicating on smart features that deliver a genuinely strong, relevant use case will make the difference between purchase or no purchase. A popular example is domestic appliances that you can switch on remotely. While this is a neat party trick, how often do we genuinely want to turn on our washing machine when we’re not standing in front of it? But it could be interesting if the machine could auto-detect fabrics, set the appropriate washing temperature and time, and send out the cycle run-time to your phone with a ‘finish’ alert.

While lack of interest ranks third globally as a reason not to buy smart appliances, this is especially true in developed markets. In developed markets, consumers tend to be more questioning about the practical benefit delivered by a piece of tech and more cautious about data protection. In comparison, in many emerging markets the population tends to be younger and more excited about owning the tech itself, and are more accepting of enjoying the benefits in return for sharing their data.

Recommendations for brands

Despite the barriers, smart products overall are set for growth. This opportunity lies in their strong alignment with three of the themes that are driving consumer purchase decisions over the next year or more: Performance, Simplification and Premiumization.

To turn consumers’ interest into conversion, brands should be focusing on five requirements that smart shoppers worldwide see as the most important.

1. Confidence & trust: Awareness must outpace consumers’ apprehensions.

It is as important to communicate the benefit and security of the smart product, as it is to have the smart feature in the first place. A compelling and clearly communicated use case allows people to feel confident that they really have a need for the product; that they will be able to use it to maximum effectiveness without difficulty, and without compromising their data security. Manufacturers and retailers should use their social media presence to promote how the product fits into daily lives to deliver greater convenience, performance or savings – using visual media such as clips and videos to catch attention. Added to this, manufactures must constantly communicate what measures they take to secure their smart products against hackers and protect users’ privacy and personal data.

2. Convenience: It makes life easier.

The device must be perfectly adapted to the user, not the user having to adapt themselves to the device. Those smart home products that have broken, or are breaking, into the mass market are the ones that go beyond being a novelty or gimmick and are unarguably useful in households – think of intruder alerts, robotic vacuum cleaners, and smart speakers. They must also be convenient to install and use. While the tech-savvy consumers may know to "do it themselves," this is not the case with the large majority. Clear messaging and proactive support on installation, choosing the best personal settings for individual circumstances, and how to get the most out of product features will all help a brand gain consumers’ trust.

3. Compatibility: It works easily with other devices in the home

The difficulty, or even inability, of getting different smart devices linking to one another has long been a source of frustration and a direct barrier for many shoppers. However, this is now being addressed with the expansion of “Matter”. Matter is a communication protocol that leverages existing technologies, such as Thread, Wi-Fi, Bluetooth, and ethernet, to allow smart devices to communicate with each other beyond the boundaries of ecosystem. It increases the interoperability of smart home devices and removes the restrictive barrier of consumers being locked in to only one brand for their smart home ecosystem. As Matter becomes more and more universal, it is expected to boost the take-up of smart products significantly.

4. Savings: It has a significant benefit over traditional alternatives (eg saving energy)

As we’ve said above, the price of smart alternatives to traditional products still remains a major consideration for many consumers. However smart connectivity can be an enabler for premium pricing when the product also offers the intrinsic value to the buyer. This can be in the form of increased performance or convenience as described above, or in long-term savings in areas such as energy use or time. The critical balance for this is that the product must be in the affordable premium range, backed by a strong, practical use case, to pull in those essential first-time buyers. This balance is the sweet spot that will increase the adoption of smart products.

My advice to retailers is to make the most of the real-time situation for marketing communications. For example, in Germany we saw a huge uptick in purchases of smart thermostats after energy prices rose sharply in Q1, with people setting up their homes against the long-term cost of living. However, the shape of the messaging must be solidly rooted in world-class data that shows the detail and nuances for your target markets and target audiences. Messaging that enraptures 20-somethings in Beijing is not the messaging that will attract 40-year-olds in New York.

----------------

Find out more about how consumers use smart tech in their homes. Our Smart Home report covers more than 25 countries, looking at people's adoption of smart devices the context of life today, the changing demands in their lives, and the unique needs and experiences of key generations.

: