min read

The tech market in Asia now leads the world, driving global economic growth. And it presents the greatest growth potential, thanks to a rapidly expanding middle class. More than 72% of APAC tech spending in 2014 was on smartphones, tablets, LCD TVs and laptops, compared to 50% of global spending.

But it’s not all good news for tech brands. As original equipment manufacturers (OEMs) and me-too's enter the market and the big name brands expand their line ups, the proliferation of options is accelerating commoditization. It’s increasingly hard for consumers to appreciate differentiation thanks to feature cloning, software standardization and product integration. It’s what we call “the paradox of choice”, the more options there are, the fewer the differences that consumers perceive. Or to put it another way, there are simply too many options and not enough choices.

Only 34% of consumers believe that smartphones have become more different to each other in the past few years. On the other hand, 46% believe that smartphones have actually become more similar. And we see a similar pattern for TVs, PCs and tablets.

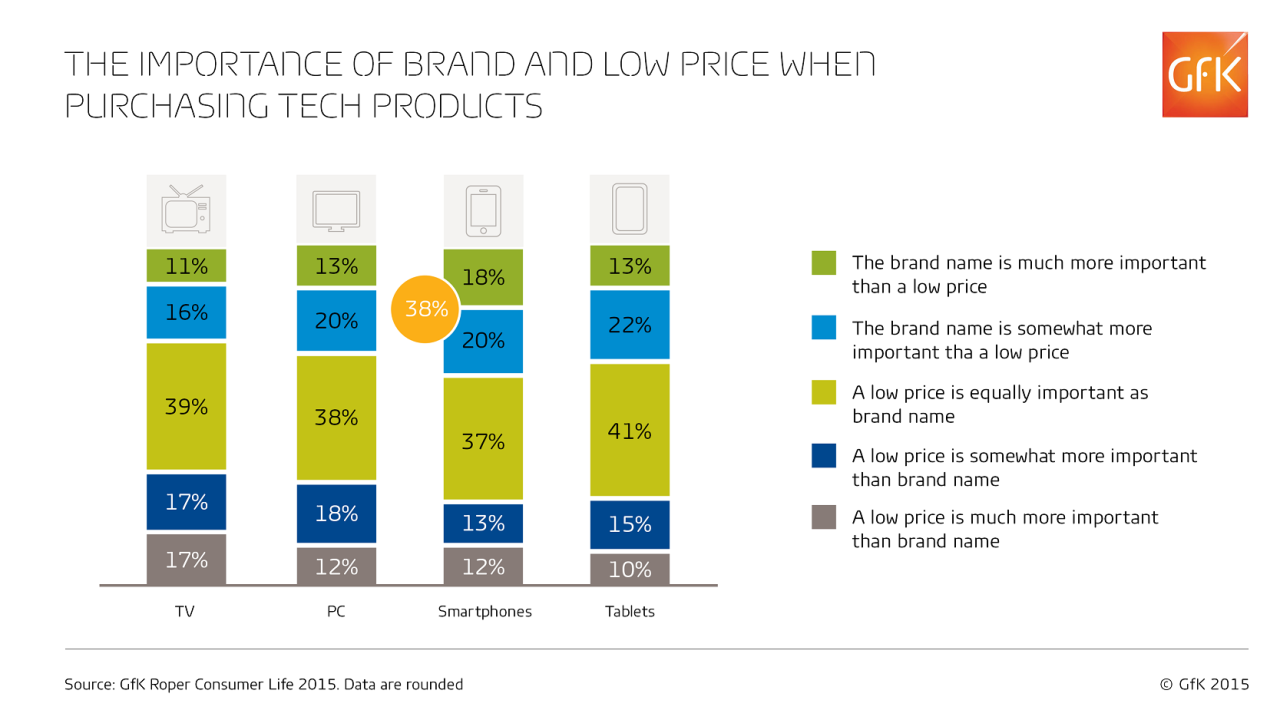

As a consequence, tech brands’ mass communications are being screened out and price is edging ahead the brand in purchase decisions. Meanwhile, retailer pressure to keep prices down and the ease of online price comparison - “e-transparency” - are ensuring that prying remains the differentiator. A low price is as important, or more important, than the brand name for 73% of TV buyers, 68% of PC buyers, 66% of tablet buyers and 62% of smartphone buyers. Meanwhile, the reactions of many companies are compounding the problem, by increasing promotions and focusing their marketing on products and in store.

It’s a real problem for the tech players because more choice doesn’t lead to more sales. We have found that typically around 25% of products generate 80% of a company’s value. When you decrease the price of those profitable units, company fortunes sink accordingly. And at the same time, brand loyalty in the developed markets is staying the same (Japan) or declining (Australia). Only one or two market leaders are able to maintain strong relationships.

“Life Brands”

Still, there is cause for optimism. The trusted brand remains a powerful draw. 72% of consumers in China only buy products or services from a trusted brand, compared to 61% globally. New software standards from the likes of Google, Apple and Microsoft should drive innovation. And emerging new tech categories such as the smartwatch create opportunities for brands to set themselves apart. Clearly too, some brands are still managing to grow and remain profitable.

It’s not the case that brands can’t transcend commoditization. And we’ve identified the shared qualities of the brands that thrive. We call these brands “Life Brands”. “Life Brands” are driven not just to sell products, but to offer a complete way of living that is supported by their products. They recognize that brands are no longer created by companies, but negotiated between companies and their consumers and that their new currency is not propositions, but sustained support. A clear social mission actively pursued over the long term is a real choice, and a reason for consumers to pick out your brand, time after time.

For more information please contact Stanley Kee at stanley.kee@gfk.com.