min read

There has been much talk about mobile payments revolutionizing payment. But what does this mean for the payments value chain?

From four parties to five

Apple Pay gained 1 million downloads within 72 hours of launch in the US. As we have come to expect of the tech giant, Apple offers a finely-crafted proposition for efficient in-store payments; now launching in the UK, it has 70% of the main banks and card issuers on board, features the neat touch of biometric authentication and takes advantage of the UK’s high number of installed NFC card payment terminals.

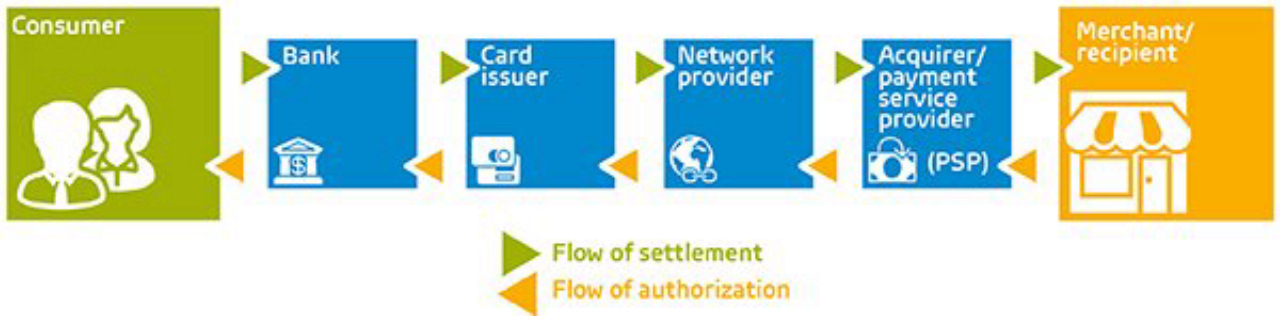

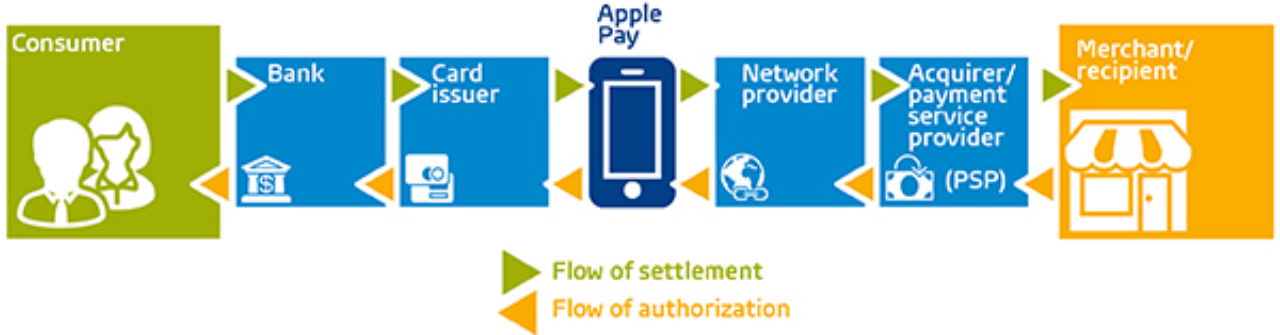

Yet while the consumer experience feels revolutionary, models like Apple Pay run on the existing card payment rails. The associated four-party value chain – bank, card issuer, processing network, merchant acquirer/PSP – for card processing is well established, hugely resilient, global in scale and trusted by consumers. No doubt these were all factors in Apple choosing to ride this well-tested route…but it also means that while payment authentication and approval is real-time, actual settlement might take several days.

Of course, by joining the established payment system – which is already under strong downward cost pressure as a result of interchange mitigation in Europe and Dodd-frank in the US – Apple Pay adds the complication of a fifth party seeking revenue from a shrinking payment profit pool.

In addition, the card issuers and banks retain ownership of the transactional data, meaning Apple Pay actually lacks the kind of reward or discount scheme which has long been seen as the key driver of mobile wallet adoption. In reality this may be a tactical move (a leaked document in the US suggests Apple does gain access to aggregated transactional data from the banks) but for now it fits well with Apple’s public position of respecting its customers’ data privacy. Customers will benefit from rewards but these will flow from the underlying card issuer schemes, not from Apple monetizing the payment data itself.

In terms of the value chain this all feels rather more like evolution than revolution; changing the form factor of the plastic card, but still relying on the plastic card architecture.

Shouldn't we be expecting something more revolutionary?

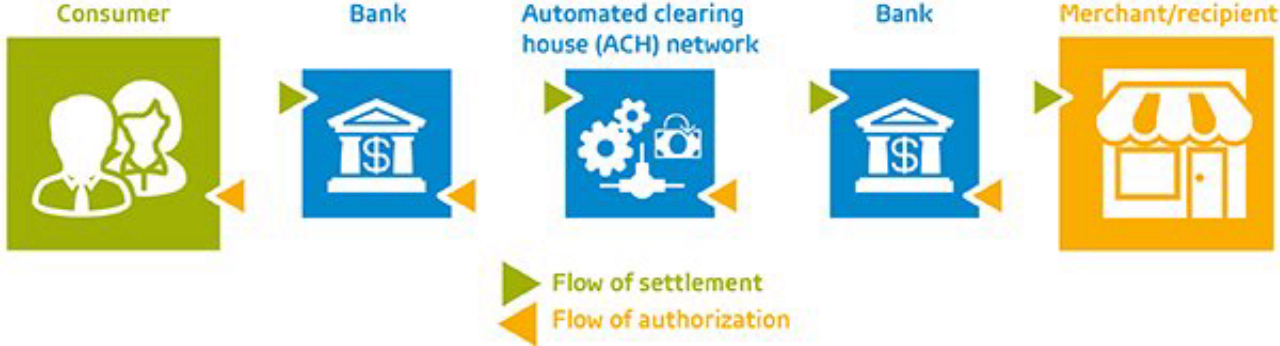

The rise of mobile has been driven by always on, instant everywhere capabilities combined with disruptive digital business models. With this has come a growing expectation of real-time functionality and of low or no-cost models, such as peer-to-peer (p2p). Set to launch in the UK this autumn, Zapp’s ‘Paybybank’ app offers both real-time settlement and much lower cost through a simplified value chain with fewer parties.

This Automated-Clearing House (ACH) model will run on the UK’s world leading real-time payment platform, Faster Payments. Recently celebrating its seven year anniversary, it already underpins p2p schemes such as Barclays ‘Pingit’ and ‘PayM’ and the inter-bank payments initiated by customers within internet and mobile banking. Zapp’s Paybybank app will extend that functionality to point of sale payments between consumers and retailers via their existing banking apps. This feels more like a revolution – the customer gets up-to-date balance information, while the merchant receives settlement much more quickly. With this streamlined system architecture, the value chain is stripped of costs. But questions remain around this model:

- How scalable is it?

There is universal acceptance of cards through the global Visa and Mastercard networks but customers (and banks) will have to trust that the Faster Payments architecture can be rolled out internationally at speed to gain similar universal acceptance. Currently, similar models exist in other European markets but these tend to differ country to country and don’t have the inter-operability of the card processing system.

- How revolutionary is it?

This model could be read as an evolutionary update on the prior card-linked model, swapping bank accounts and a clearing house for plastic cards and card processors.

What else is on the horizon for the mobile payments value chain?

The regulatory agenda in Europe is picking up further pace with Payment Services Directive 2 (PSD2) which aims to provide open access to the transactional data itself. Previously owned exclusively by the card issuers, PSD2 will allow approved payment providers to gain access to the personal transactional data which is increasingly being recognized as the most valued part of the payments value chain. Expected to reach member states in 2017, PSD2 potentially unleashes huge disruptive power to new payment services providers and reward scheme operators, providing they can win users trust and gain scale with sufficient speed.

Looking beyond the developed world more revolutionary value chains already exist, fueled by differing infrastructure landscapes. 13 countries in sub-Saharan Africa have more mobile phone accounts than bank accounts, lending rise to the development of mobile money – digital cash stored directly on mobile phones and available to fund point of sale payments. Vodafone’s M-Pesa has famously succeeded using this model in Kenya but huge potential exists in other markets where banking and payment infrastructures lag mobile network infrastructures.

Also brought into the media spotlight in Greece as the banking system froze up (as was also the case with Cyprus) is the potential for the distributed ledger/blockchain model to remove banks and traditional financial service providers from the value chain altogether. However, Citibank’s recent revelation that they ‘have been exploring distributed ledger technology for years’ underlines the fact that disruptions to the payments value chain are unlikely to catch the financial industry by surprise.

For more information please contact Ian Davis at ian.davis@gfk.com.