min read

5% - this is the percentage of all payments made globally, in a store, using a mobile device last year. So, why should anyone care? Put simply, in-store mobile payments are the future. Yes, there are barriers – logistics and security are the main ones – but there are also opportunities for businesses and consumers. Mobile payments will offer a faster and more convenient way to pay on a daily basis. It will also create a more innovative rewards system than is currently offered by the cards that we carry with us every day. There are, however, a number of hurdles on the path to widespread adoption.

Knocking down the barriers

There are a number of barriers that need to be overcome before mobile payments are the norm. One of these challenges is logistics. This problem can be broken down into three parts:

- The technical aspect. While Apple, Google, and Samsung (to name a few) have wallet apps – not all consumers have devices capable of supporting the payment technology needed to use these in store. However, this technology is evolving rapidly and more retailers (such as Target in the USA and Boots in the UK) are starting to install readers for Apple Pay and NFC (Near Field Communications) for use with Android devices.

- Company partnerships. Technology, financial, and retail companies are all looking to profit from mobile payments - and compromises will no doubt need to be reached. These relationships are tricky to arrange and will redefine traditional payment chains. However, several partnerships already exist. For example, Apple Pay is growing with retailers in the USA and will launch in the UK in July. In the UK, Apple already established several partnerships with banks (HSBC, Royal Bank of Scotland, Lloyds Bank, and Santander) and retailers/service providers (Boots, Nando's, Waitrose, and Transport for London).

- Educating consumers. Younger generations are more interested (41% of Millennials vs. 18% of Baby Boomers) and more willing to accept new technology, while older generations tend to be more hesitant. In addition to a willingness to adopt, consumers of all ages will need to transition to a point where the majority own a device that is capable of an in-store payment. Moreover, security must evolve to support consumers in paying for both everyday and non-everyday items. Technological advances and the economic benefits will help resolve the logistical challenges. Security, however, is a greater barrier.

Resolving the security problem

Almost anything published on mobile payments will highlight security as the main barrier to the widespread adoption of this technology. But, security has always been and will always be an issue when an individual parts ways with personal information and money. And, while it cannot be ignored, it can be overcome.

Establishing trust is vital to alleviating concerns about data protection and financial loss that surround mobile payments. Beyond legislation designed to protect consumers, companies across all sectors must demonstrate that this is a safe way to pay. Part of that trust comes from the current financial reliance that consumers have on banks and credit card companies. Security options such as passwords and biometric authentication will also provide reassurance. However, technology and financial organisations need to go a step further by offering consumers control over what they opt into. Ultimately though, it may be consumer curiosity and convenience that supersedes security concerns.

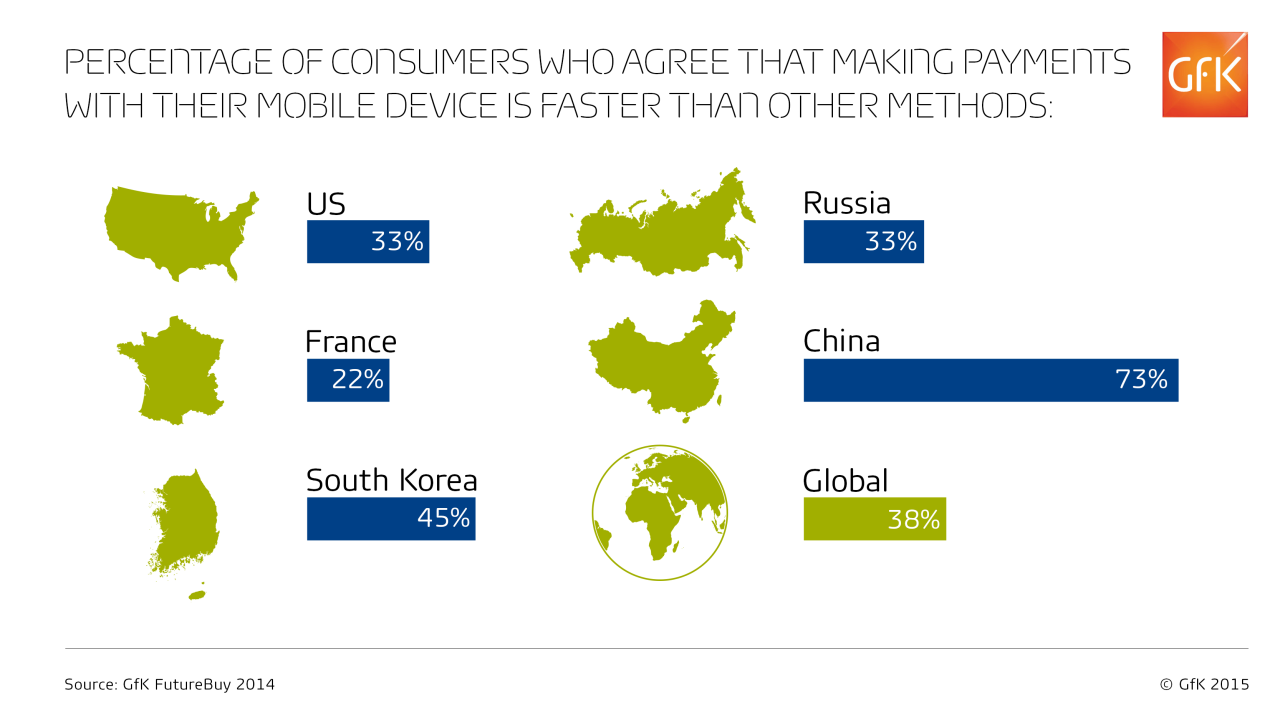

Mobile payments are convenient

In October 2014, 29% of US consumers said that they intended to make a mobile payment in store in the next 12 months, and, 33% thought it was faster to pay this way. Convenience and speed are big advantages and consumers may start to worry less when presented with an easier payment method that is underpinned by brands they trust. That said, convenience is not enough to support the argument that in-store mobile payments will be a way of life. Consumers already have card options that are both easy and quick to use. Mobile payments, however, has an advantage over cash and cards, which is that it can interact with the consumer.

Rewarding consumers – the advantage of mobile payments

Rewards, loyalty schemes and instant discounts are what consumers will gain from mobile payments. Retailers could offer consumers discounts when they are in or nearby a store using the individual’s location. Alternatively, if a retailer knows a consumer has been browsing for something online, they could text them a discount code to use in store or alert them to a deal through an app. Furthermore, mobile payments will eliminate the need for paper coupons and plastic reward cards. Beyond instant discounts and convenience, consumers also have the option to cap and monitor spending.

While there are logistical and security barriers to overcome, mobile payments will revolutionize the way consumers, retailers, financial institutions and technology companies interact. As consumers get to grips with the technology and understand how it benefits them and as companies increasingly see the opportunity to profit, mobile payments will become widely accepted and will ultimately replace cash and cards.

All data from the GfK 2014 FutureBuy Study. The 2015 FutureBuy Study will be available in the Autumn of 2015.