min read

Europe's economy has again gained momentum. Increased domestic demand as well as improved external competitiveness, particularly in several of the economically weakened countries, can contribute to more balanced, sustainable growth to the benefit of retail. While this overarching assessment is positive, the situation varies starkly at the regional level.

We have just completed a comprehensive analysis of the European retail scene in 32 European countries. The study examines purchasing power, the retail share of the population's total expenditures, inflation, sales area productivity, changes in retail due to eCommerce, as well as a turnover prognosis for 2015. Here are some results:

- Purchasing power: A total of approximately €7.75 trillion was available to consumers in the EU-28 countries in 2014 for spending and saving. This corresponds to a per-capita purchasing power of €15,360, which is a nominal increase of approximately 2.5 percent compared to 2013. But a vast prosperity gap continues to persist in Europe: While Norway has a disposable per-capita income of €30,560, Bulgaria has just €3,097, which is around one-tenth of the Norwegian figure.

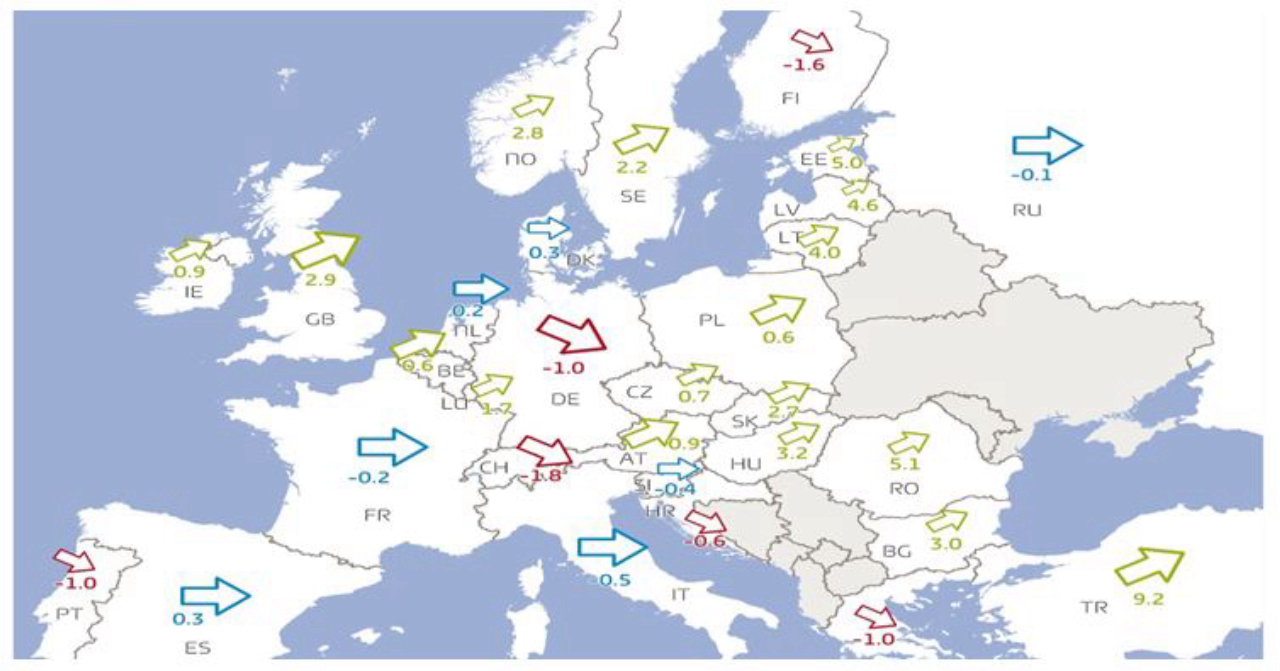

- Turnover prognosis: Growth in online trade is placing increasing pressure on stationary retail throughout Europe. GfK therefore forecasts only moderate nominal stationary retail growth of just 0.5 percent in 2015 across the EU-28 countries. This amounts to an average growth of 0.8 percent when all 32 evaluated countries are taken into account. Notable frontrunners again include Romania (+5.1 percent) and the Baltic States (+4.0 percent to +5.0 percent). In 2014, the retail situation began to stabilize in the southern European countries strongly impacted by the economic crisis. However, retail turnover will again decline in Greece. On the basis of the currently available data for 2015, and assuming Greece does not secede from the European Monetary Union, this decline is expected to remain modest at around -1.0 percent.

- Retail share of private consumption: The retail share of private consumption fell again in 2014 among the EU-28 countries to 30.9 percent (2013: 31.2 percent; 2012: 31.4 percent). This development was influenced by two key factors with conflicting effects: first, the fall of oil prices in mid-2014, which resulted in decreasing costs for energy and fuel; and second, the long-standing trend toward ever higher spending on accommodation, health and recreation. These expenses translate to less money available for retail consumption and ultimately supersede the short-term effect of falling oil prices.

- Inflation: Consumer prices climbed only moderately in 2014 (+0.6 percent), and an inflation rate of just 0.2 percent is forecasted for 2015. For 2015, the European Commission even expects deflationary tendencies in some countries, with the greatest effects predicted in Spain and Switzerland at -1.0 percent apiece. The highest rates of inflation will again be in Turkey (+6.3 percent) and Russia (+6.0 percent). Due to the low inflation, real-value turnover for stationary retail is anticipated to remain stable in 2015.

- Sales area productivity: In many countries, sales area productivity has begun to increase again after delays to many projects occasioned by the financial crisis. Among the EU-28 countries, sales area productivity has climbed by 0.6 percent to around €4,100 per m2. Luxembourg, Switzerland and the Scandinavian countries again top the list of countries in 2014 with the highest sales area productivity. The countries with the lowest sales area productivity are located in Eastern and Southeastern Europe. Thanks to the positive development in turnover in the majority of these countries, overall sales area productivity nonetheless increased here in 2014.

- Changes caused by eCommerce: GfK observes that sales area productivity is increasingly under pressure in Northern and Southern Europe, particularly in Germany, France and Great Britain. A major reason for this is the redirection of turnover to Internet retail among many product lines. Although eCommerce has significant momentum in Eastern Europe, the effects are not yet having a strong impact, because the absolute volumes being transacted over the Internet are comparatively small. Poland is a prime example. By contrast, in mature markets such as Germany, segments such as clothing retail are no longer as expansive as they were several years ago. At the same time, the number of shopping centers that are planned or under construction is decreasing, which is both a cause and effect of the changed market dynamic.

More information

The study can be downloaded for free as a PDF at www.gfk.com/european-retail.

Dr. Gerold Doplbauer is GfK retail expert and lead this study. He is also the team leader of the Real Estate Advice department within GfK’s geomarketing division.

Contact him at Gerold.doplbauer@gfk.com.