min read

The use of mobile payment is in its infancy in Belgium, yet awareness is relatively high. Our latest research highlights some of the obstacles to widespread adoption, and suggests how the market might develop in the future.

Our FutureBuy study of 17,000 consumers across 17 countries identifies that just 5% of transactions are made using a mobile device. Although cash and cards are still used for the majority of transactions across these markets (46% and 45% respectively), there is an enthusiasm to pay via mobile. Two barriers are preventing widespread adoption – the two “Ts” of trust and technology. The picture is similar in Belgium, but here it would appear that mobile payment seems to be very much a youth market phenomenon.

Assessing awareness

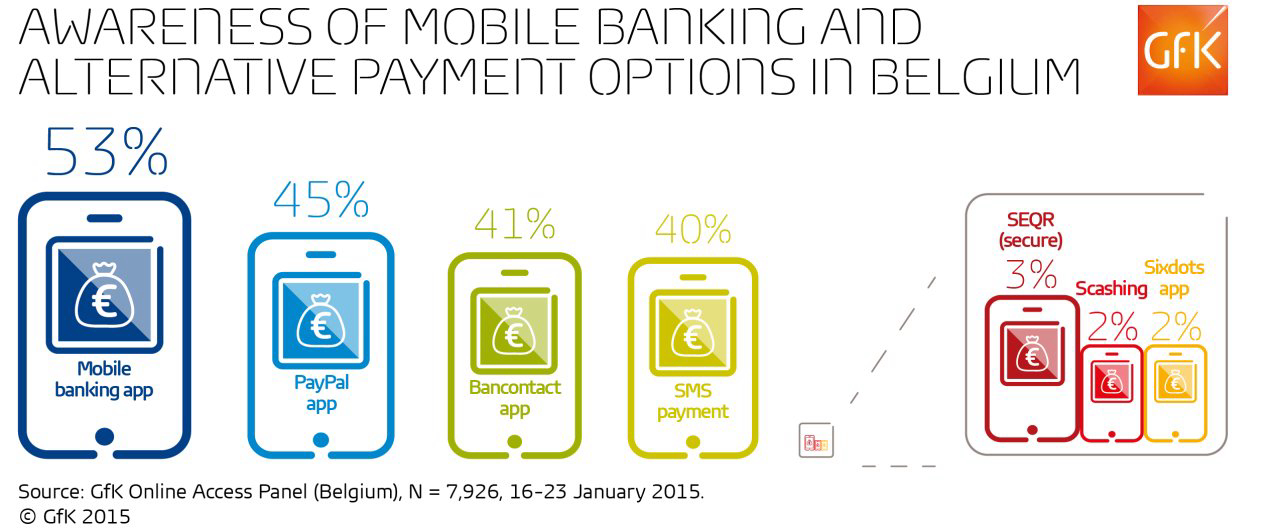

There’s no question that awareness of mobile banking is relatively high in Belgium with more than half (53%) of consumers knowing about banking apps. Knowledge of alternative payment options to using cash and cards was also relatively high: 45% knew of PayPal’s app, 41% of Bancontact’s app, and four in ten (40%) of SMS payment. As the leading national debit card provider, it’s perhaps no surprise that Bancontact’s mobile payment solution is so well-known. SMS payment alsoenjoys widespread adoption as it is integrated across the country’s public transport network and parking spaces. By comparison, new players or initiatives including SEQR, Scashing and Sixdots have little to no awareness and all score under 5%. Awareness of these brands in general is higher amongst younger consumers, the higher social grades, and in the Flemish region.

Bancontact clearly has a strong brand and consumers trust it with their debit card payments, suggesting their app could unlock the Belgian mobile payments market. Yet there are companies, the two best known being McDonalds and major retailer Colruyt, that have agreed to partner with SEQR. This app currently has an awareness of less than 5%, but this could change soonif all involved in this partnership collaborate to ensure this payment solution is adopted.

Younger consumers are leading the way

We wanted to understand what the experience of paying via mobile was like in Belgium. We saw a big gap based on age. One third (34%) of people aged 25-34 who have left home have used mobile payment in the last year at least once. The figure drops with age, with only 18% of those aged 45 and older using it. The average is two in ten (21%). Only one quarter of people (25%) are planning to pay more via mobile in the coming year.

Transferring funds, either to other people or businesses, is used by one quarter (25%) of 15-35 year olds, but only 15% of the total population. On the other hand, SMS payment, which is a more accepted and popular means of paying for public transport and parking, is used by one third (33%) of all consumers, rising to almost half (48%) of 15-24 year olds.

Towards a tipping point

Our research points to some of the challenges posed by the two “Ts” to wider take up of mobile payment in Belgium. However, there are motivations for paying this way. The lead reasons being speed (41%), and convenience (36%). With 28% of people saying they would like to see more mobile payment options in traditional stores, the major retailers need to work together to overcome the challenges and facilitate payment in their stores to help drive usage. Not only do they need to focus on rolling out the “technology”, but they also need to explain its benefits and reliability to garner consumers’ “trust”. Almost two thirds (64%) of people in our research cited their belief that mobile payment technology was still in development as a reason for not using mobile payment.

Privacy and safety concerns are also a motivation for not using mobile payment. Seven in ten people (70%) are concerned about their privacy when paying by mobile, and half (48%) believe mobile payment is less secure than other ways to pay. This explains why four in ten Belgian respondents (44%) have said they would be more likely to use mobile payment if it was for smaller sums. It is worth remembering that consumers have plenty of other options to pay for goods and services, so clearly there is a lot of work to do in communicating the measures taken to guarantee both personal privacy and security of mobile transactions before the country experiences broader take-up.

Summary

At present, in Belgium there seems to be a genuine disconnect between what the retailers are doing and what consumers want and are willing to do. If retailers and payment providers don’t collaborate, there is a possibility that groups of stores and outlets will use a range of different payment mechanisms, increasing the threat of fragmentation. Consumers are not going to install five different mobile payment apps to pay via mobile in five different stores simply because it suits the retailers. By working together, retailers have the opportunity to come up with a solution that works for everyone.

Source: GfK Online Access Panel (Belgium), N = 7,926, 16-23 January 2015.

For more information, please contact us.

For further insights and benefits from the world of digital and more about our offerings, visit our Digital Market Intelligence pages.