min read

This is a summary of our white paper “A Rising Stream Lifts… Lessons from the New TV Marketplace”. To read the whole paper click here.

The accelerating growth of subscription streaming video services in the USA, such as Netflix, Amazon Prime, and Hulu Plus, has added more confusion to an already challenging media marketplace. Facing off against these “streamers” are TV service providers which are fighting to maintain their piece of the subscription pie – often with streaming offerings of their own. The result is a dizzying landscape of constantly changing players and partners.

Watching streaming video has clearly become a habit beyond the “early adopter” crowd. We recently found that almost half (46%) of all Americans aged 13 to 54 view TV programs or movies over the internet at least once a month, using any type of streaming. And a third (34%) of all 13 to 54 year olds are monthly users of a pay streaming service, a figure driven predominantly by Netflix.

TV service providers have since launched a variety of services – with TV Everywhere (TVE) and Video-on-Demand (VOD) playing key roles. Hoping to hang on to “traditional” audiences once they leave the linear TV broadcast, TVE and VOD offer current program episodes and home movie releases that are not available from subscription streaming services. The combination of TVE and VOD offers a way to differentiate a TV provider through an added-value offering, allowing it to be seen as not just a delivery system, but also a curator of exclusive content

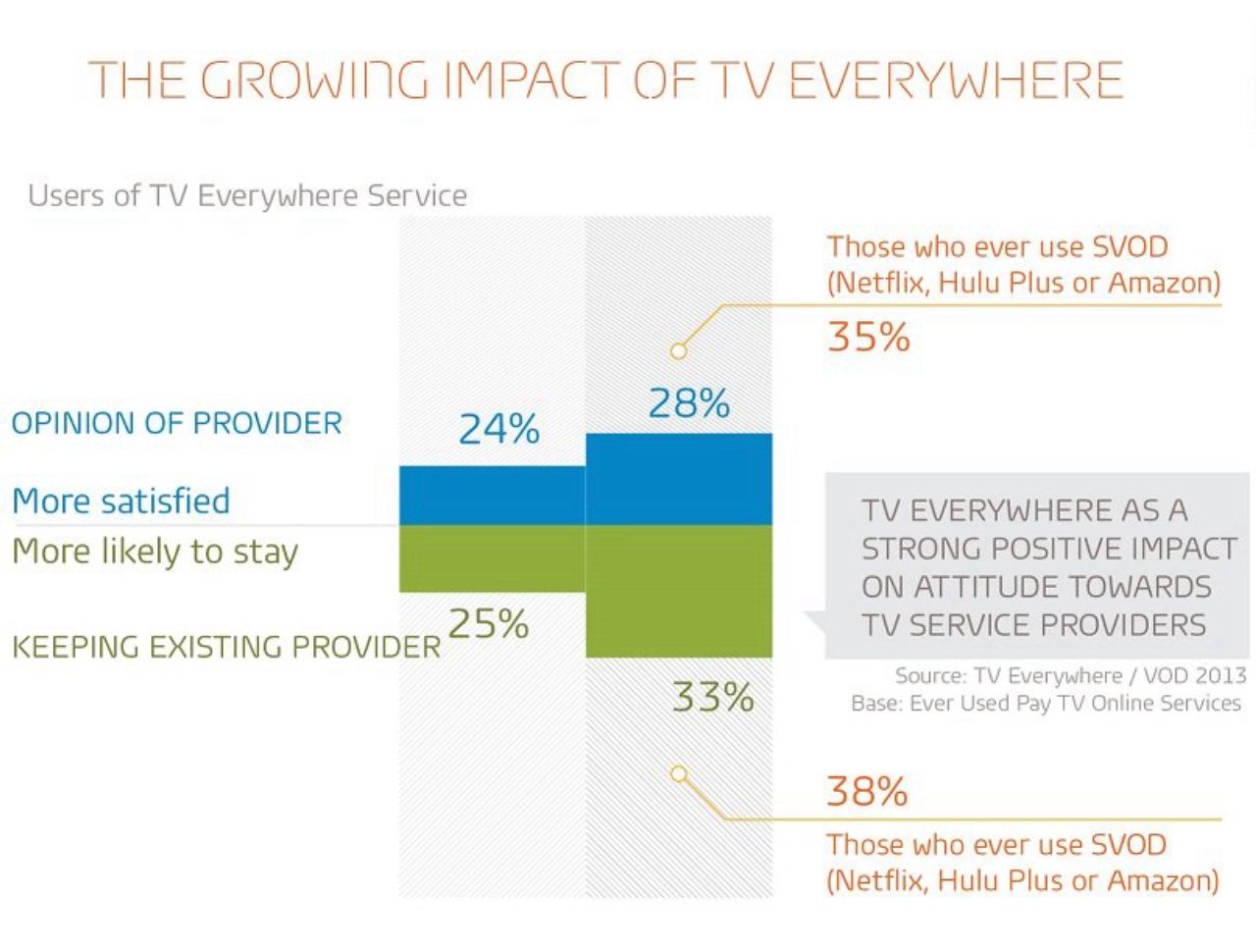

All the while, there is evidence that TVE is falling victim to a historical weakness of cable company offerings that also stunted the potential of VOD: the lack of consistent messaging to consumers, resulting in low awareness, understanding, and use. This is less of an issue for “national” TV services such as satellite, since they can offer the same branded TVE name everywhere. Although each operator wants to have its own nomenclature, a standardized logo or tagline (for example, “Intel Inside”) would help consumers understand what’s being offered, while providing the opportunity for brand differentiation that operators crave.

Windows of opportunity for TVE, VOD

Our 2013 data shows that almost half of Netflix subscribers would be willing to switch to a similar service from their TV provider, were it offered at the same cost. The TVE/VOD combination has the advantage of offering current network episodes and new movie releases, something subscription streaming services generally don’t have. The key value to subscription streaming services is their access to catalog content and “all past seasons” episodes. If TV providers can negotiate for more catalog content and stacking rights, this advantage can also be negated.

There is still a tall mountain to climb for TVE and VOD. Though a plurality of those who use both VOD and subscription streaming video services prefer streaming services, there is hope for winning the hearts and minds of viewers if they can be convinced to try VOD on a consistent basis. For those who use VOD at least weekly, the results flip. This emphasizes the potential opportunity if the TVE/VOD combination is successfully marketed.

Strategy for the future

TV networks and TV service providers alike should be congratulated for their proactive entries into the non-linear viewing space. By extending their relationship with their viewers past the TV set and placing branded services onto mobile devices, these partners in the traditional TV world are battling head-on against strong streaming-only challengers.

So how should these different players look to secure their futures in this competitive environment?

- TV service providers must avoid becoming a “dumb pipes” that just deliver internet video from other sources and services

- TV networks need to differentiate themselves from the already-long list of amorphous video aggregators. How can they leverage their brand and content quality to be the first place people turn for video entertainment?

- Streaming services must look at evolving their current pricing models in order to maintain the low cost that drive their subscriptions

- Content creators must also look to solutions for supplying “analog era” quality content at “digital era” price points

For related content, visit our dedicated Mobile World Congress site.

Source:

GfK How People Use® Media: Over-the-Top TV 2013. USA sample only

GfK How People Use® Media: TV Everywhere/VOD 2013. USA sample only

Email the author: david.tice@gfk.com